Economic growth is an increase in national output/income (higher real GDP).

There are two main aspects of economic growth:

- Aggregate demand (AD) (consumer spending, investment levels, government spending, exports-imports)

- Aggregate supply (AS) (Productive capacity, the efficiency of economy, labour productivity)

To increase economic growth

We need to see a rise in demand and/or an increase in productive capacity:

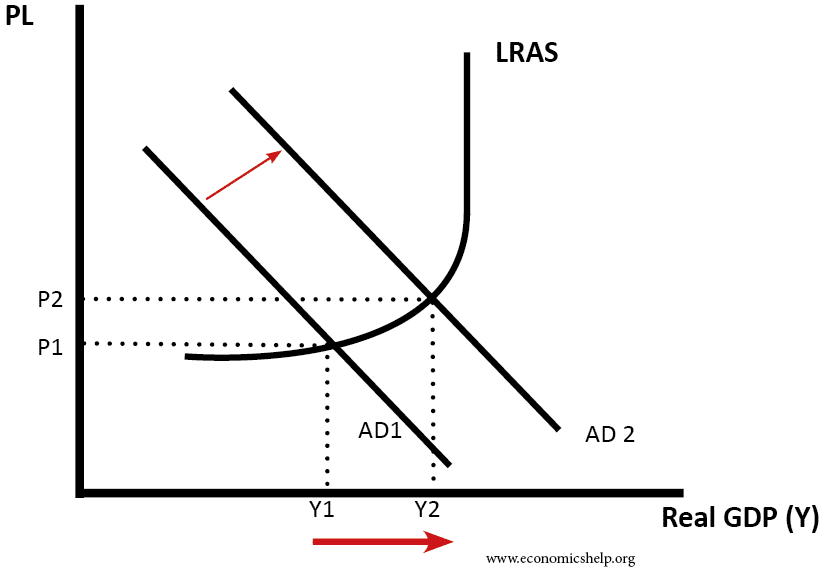

1. A rise in aggregate demand

Aggregated demand can increase for various reasons.

- Lower interest rates – reduce the cost of borrowing and increase consumer spending and investment.

- Increased real wages – if nominal wages grow above inflation then consumers have more disposable to spend.

- Higher global growth – leading to increased export spending.

- Devaluation, making exports cheaper and imports more expensive, increasing domestic demand.

- Rising wealth, e.g. rising house prices cause consumers to spend more (they feel more confident and can remortgage their house.

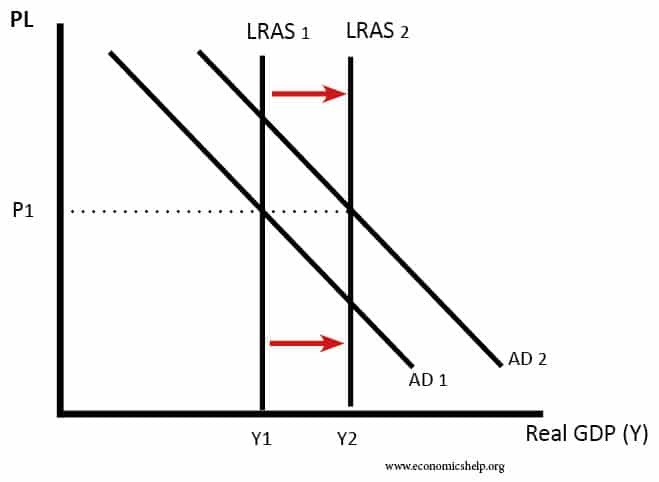

Growth in productivity

This is growth in aggregate supply (productive capacity). This can occur due to:

- Development of new technology, e.g. steam power and telegrams helped productivity in the nineteenth century. Internet, AI and computers are helping to increase productivity in the twenty-first century.

- Introduction of new management techniques, e.g. Better industrial relations helps workers become more productive.

- Improved skills and qualification.

- More flexible working practices – working from home, self-employment.

- Increased net migration – especially encouraging workers with the skills that are in short supply (e.g. builders, fruit pickers)

- Raise retirement age and therefore increasing the supply of labour.

- Public sector investment – e.g. improved infrastructure, increased spending on education and

To what extent can the government increase economic growth?

A government can try to influence the rate of economic growth through demand-side and supply-side policies,

- Expansionary fiscal policy – cutting taxes to increase disposable income and encourage spending. However, lower taxes will increase the budget deficit and will lead to higher borrowing. The expansionary fiscal policy is most appropriate in a recession when there is a fall in consumer spending.

- Expansionary monetary policy (now usually set by independent Central Bank) – cutting interest rates can boost domestic demand.

- Stability. A key function of the government is to provide economic and political stability which enables the usual economic activity to take place. Uncertainty and political tension can discourage investment and economic growth.

Government supply-side policies

- Investment in infrastructure, e.g. new roads, railways lines and broadband internet – increases productive capacity and reduces congestion.

- Privatisation and deregulation – increase efficiency and productivity.

Factors beyond the government’s influence

- The rate of technological innovation tends to come from the private sector and it is hard for the government to influence this.

- Industrial relations and workers motivation are driven by the private sector. The government’s influence on worker morale and motivation is limited at best.

- Entrepreneurs who set up a business are largely self-motivated. Though government regulations and tax rates can influence the willingness of an entrepreneur’s willingness to take risks.

- Level of savings can influence growth (e.g. see Harrod-Domar model) Higher savings enable higher investment, but it can be hard for the government to influence savings.

- Willingness to work. In the post-war period, the defeated countries Germany and Japan saw rapid rates of economic growth – reflecting a determination to rebuild after the war. UK economy had less dynamism – this could reflect different attitudes to work and willingness to introduced new ideas.

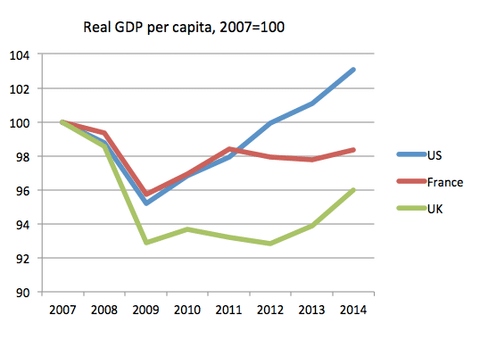

- Global growth exerts a strong influence on any economy. If the world enters a global recession, it is very hard for an individual economy to avoid the costs. For example, the credit crunch of 2009 negatively affected economic growth in OECD economies.

US, France and the UK all entered the recession in 2009. However, the better recovery in the US could be due to different policy responses. Expansionary fiscal policy of 2009/10 and a looser monetary policy.

Governments often over-estimate how much they are able to increase productivity growth. Most of the technological progress comes from private sector without government intervention. Supply-side policies can help increase efficiency to some extent, but it is debatable how much they can actually increase growth rates.

For example, after supply-side policies of the 1980s, the government hoped there had been a supply-side miracle which enables a much faster rate of economic growth. However, the Lawson boom of the 80s proved to be unsustainable and the UK growth rate remained pretty much the same at around 2.5% At the very least supply-side policies will take substantial time, e.g. increasing labour productivity through education and training will take several years.

For developing economies with substantial infrastructure failures and lack of basic amenities, there is much greater scope for the government increasing growth rates. By providing basic levels of education and infrastructure the scope for higher growth rates is much higher.

Most productivity growth is determined by the private sector. With a few exceptions, most technological improvements come from private firms. It is the private sector which develops new technology which enables the vast majority of productivity growth we see in the UK. I’m sceptical of the government’s ability to invest in new technology which would boost this rate of productivity growth. (though it can happen – especially in war)

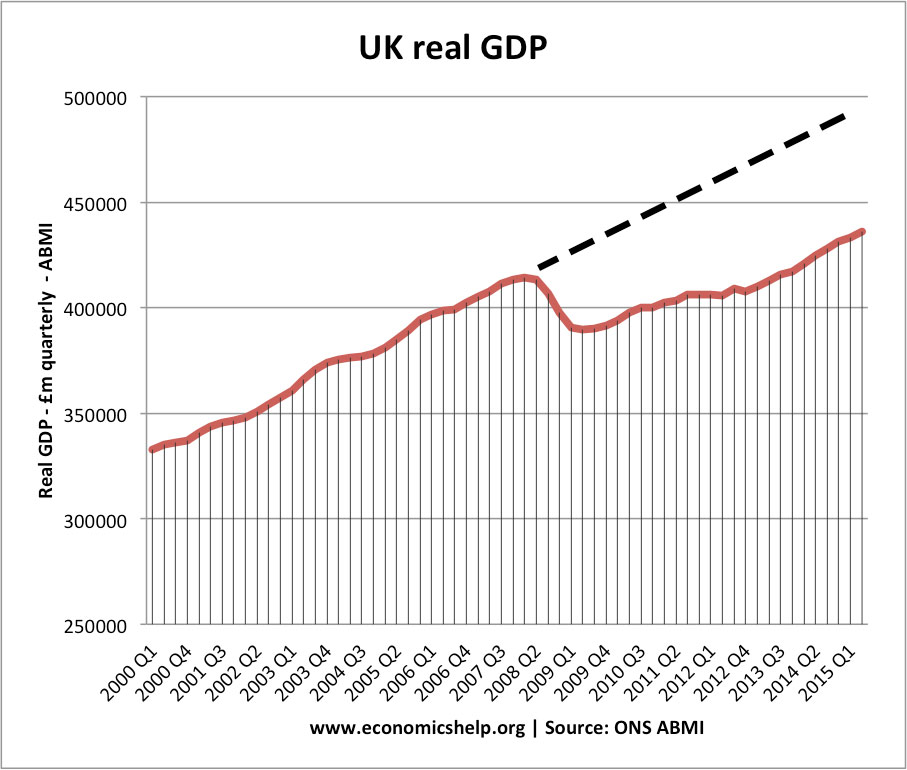

Economic growth in the UK

Since 1945, the UK economy has grown by an average of 2.5% a year. Most economists would argue that, on average, the UK’s productive capacity can increase by around 2.5% a year. This is known as the ‘trend rate of growth’ or ‘underlying trend rate’.

Note, even when the government tried supply-side policies, they usually failed to shift this long-run trend rate. (e.g. supply-side policies of the 1980s, did little to alter the long-run trend rate)

The graph below shows how actual GDP fell below the trend rate from 2008. This was due to the recession and a significant fall in Aggregate Demand.

Growth in productive capacity (AS) occurs because of:

- Improved technology developed by the private sector which enables higher labour productivity (e.g. development of computers enables greater productivity)

- Improved management techniques which enable a more skilled workforce.

- Improved education and training by both private sector and public sector

- Investment in infrastructure, e.g. building new roads and train lines. This is mainly the responsibility of the government.