By the end of 2013, the UK government will have implemented 52% of planned fiscal consolidation. The IFS report that most of this fiscal consolidation has come through taxes. In coming years, we will see the impact of cuts to the benefit budget. Only 58% of the total cuts to benefit spending have been implemented, …

There is mixed evidence about the success of the Funding for Lending scheme Firstly, there is evidence that credit is still tight and firms are struggling to gain finance. Since last August, £1.8bn of credit has been drained out of the system At the same time, up to 40 lenders have accessed the £16.5bn in …

Latest GDP statistics show economic growth of 0.3% in Q1 of 2013. (Link ONS) The strongest growth has come from the service sector (1.3%) and retail in particular. Production industries fell -2.6% in Q1 2013. Construction was hardest hit falling – 6.3% Despite the strongest growth in real disposable income since 2009. (Real household disposable …

In the past few years, Central Banks have been buying bonds to

Increase money supply

Reduce bond yields

The aim of quantitative easing is to avoid deflationary pressure and increase economic growth. Ending quantitative easing will mean The Central Bank stop buying any more bonds. The process will then be reversed and, in time, the Central Bank will start selling the government bonds that they have.

The implications of this will be:

Falling bond prices and rising bond yields. Q.E. has had the effect of making bonds more attractive. Demand has been boosted by the Central Bank intervention, and this has encouraged investors to buy bonds (also helped by the relative security of bonds during a recession) However, when the Central Bank sell bonds, the price will go down, and this has the effect of increasing bond yields.

It is not just the Central Bank who will sell bonds. The fear is that when the markets see the Central Bank is ending Q.E. they will sell bonds because they know the market is turning. This is shown by the fact that bond yields rose following just an announcement from Federal Reserve that Q.E. may end ‘at some time in the future’

Money supply. If banks buy bonds from the Central Bank, they will see a fall in their cash reserves, and in theory, this could lead to lower bank lending as they maintain liquidity reserves.

However, this effect may be very limited because quantitative easing in the first place didn’t really encourage any increase in bank lending. Banks just sat on their increased reserves. Arguably we have had the wrong ‘type’ of quantitative easing – but that is another question.

When interest rates were cut to 0.5% in March 2009, few would have expected them to remain at 0.5 until the present time. Yet, we have seen an unprecedented period of zero interest rates. There is much speculation about:

When interest rates will rise?

How much will interest rates to increase to?

What will be the effect of rising interest rates on an economy, that has got used to low interest rates?

When will interest rates rise?

Essentially interest rates will rise when there are signs of a strong economic recovery, which is starting to cause the threat of demand pull inflation. The problem is that, over the past few years, the UK has seen many ‘green shoots’ of recovery which have failed to translate into a lasting recovery. In recent months, retail sales have improved – indicating some signs of recovery, but the EU recession is holding back recovery, creating a patchy picture. Policy makers will want to see annualised growth of 2.5% a year before there is greater confidence that the UK is leaving the this era of stagnant growth.

Important factors in signalling an end of zero interest rates

Signs of core-inflation. The main motivation for raising interest rates is to prevent a return of inflationary pressures. If core inflation (which strips out volatile factors) starts to increase above 2%, then there will be a strong case to increase interest rates. In Europe and US, inflation is actually falling to below 1.5%. The UK headline inflation rate is higher, but during the great recession, the Bank of England have correctly been suspicious of the CPI rate. It hasn’t a true reflection of demand pull inflation – more a reflection of cost-push factors.

Wage inflation. A key sign for a return to economic normalcy, will be an increase in real wages. Currently nominal wage growth is very weak. Many workers are seeing wage freezes. In this climate of real wage cuts, economic activity is depressed and the case for higher interest rates remains very weak.

Fall in unemployment. The US and UK have seen moderate falls in unemployment levels, but unemployment is still significantly above the natural rate (structural unemployment). Whilst there remains demand deficient unemployment, there is a case for keeping monetary policy loose (low rates). Also, there is a well-grounded fear that unemployment rates offer a slightly better picture than reality. Unemployment figures have been masked by a rise in under-employment.

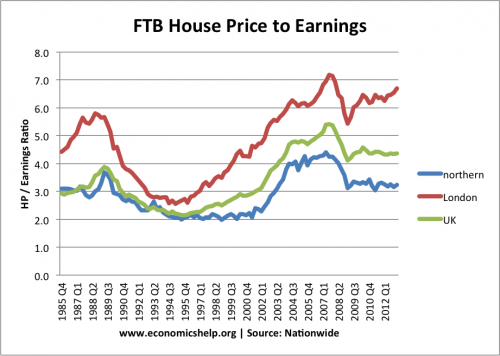

Any sign of boom in the housing market. An increase in house prices could restart a round of higher spending, driven by the ‘wealth effect’ However, in the UK, house prices still look overvalued on ratios of house price to incomes. A fall in house prices may be more likely than rising house prices.

How much will interest rates increase?

This is an interesting question. Pre-crisis, ‘normal interest rates’ may have considered to have been 5% There is a widespread assumption that a return to trend rate growth of 2.5% and inflation of 2%, would see interest rates of 5% – giving us a more normal real interest rate.

However, as Mervyn King recently pointed out, many young homeowners have borrowed extensively to get on the property ladder.

Expensive house prices

A small increase in interest rates will significantly increase the cost of mortgage payments, and therefore a small increase in interest rates will have a large impact on reducing economic growth. (see more housing stats) Because we have got used to low interest rates a small increase will have a big impact on the economy. In other words, the UK is particularly sensitive to interest rates. If interest rates increased to 5% quickly, it would have a large contractionary effect – which would end the nascent recovery. Therefore any increase in interest rates to prevent inflation can be relatively small.

Containerisation is a system of standardised transport, that uses a common size of steel container to transport goods. These containers can easily be transferred between different modes of transport – container ships to lorries and trains. This makes the transport and trade of goods cheaper and more efficient. The container was invented in 1956 by …

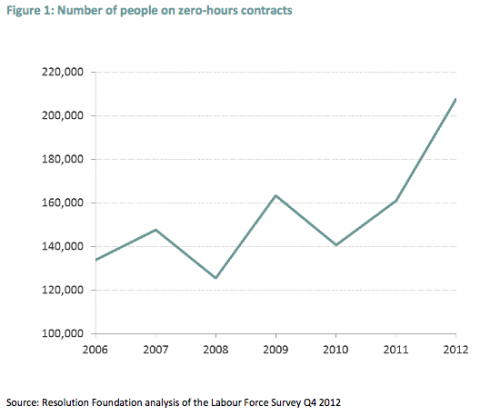

One feature of the labour market in the past 10 years has been the rise of zero-hour contracts. This is a contract where the employer is not obliged to employ a worker for any number of fixed hours. It means that the contract is highly flexible in terms of hours worked. This is obviously advantageous for an employer who has fluctuating demand and who seeks to cut the wage bill in quiet periods.

Flexible working hours can have benefits for some types of workers, e.g. students or second income earners who like the flexibility of doing different amounts of hours from week to week. Some also credit flexible working practises for limiting the rise in UK unemployment during the recent recession.

However, for many workers, zero hour contracts have greatly increased the uncertainty of work. It means, in quiet periods, many workers can be left with insufficient income to meet monthly bills. This increased labour market flexibility, thus comes at a cost of increased uncertainty and lower-income.

Home repossession – when banks take homes back into their own ownership,

Mortgage arrears – when mortgage holders fall behind in their mortgage payments, but not necessarily leading to repossession

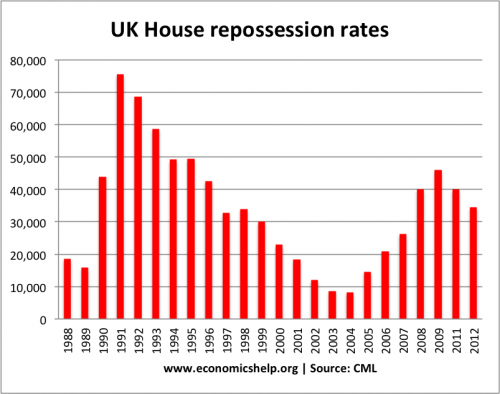

For 2013, the Council of mortgage lenders anticipate a total of 35,000 repossessions. In Q1 2013, the rate of repossession is running at 0.07% or 1 in 1,400 homes. This is the lowest rate since 2008. (Source: CML)

In 2012, 157,900 homes were in arrears.

It estimated, that 160,000 mortgages will be in arrears of 2.5% or more by end of 2013.

This repossession rate of 0.07% is significantly lower than the last housing bust and recession of 1991-92. In that period, the repossession rate peaked at 0.7% of homes.

Why is repossession rate low during credit crunch?

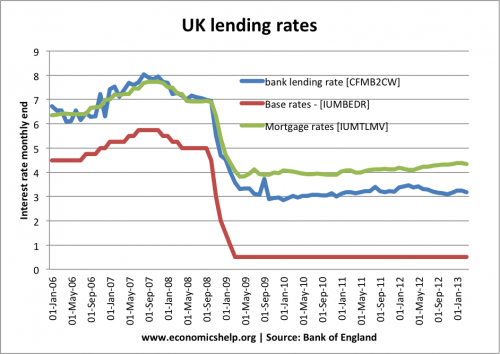

Low interest rates. The main difference between the 1991 crash and the great recession 2008-13 is the difference in interest rates. In 1992, the government increased interest rates to 15% in an attempt to reduce inflation. Unsurprisingly, these high interest rates caused many homeowners to be unable to afford mortgage repayments, and so the repossession rate increased. In 2013, we have had a period of very low interest rates since March 2009. Base rates are 0.5%. Homeowners on tracker mortgages are facing very low mortgage payments. Fixed rate mortgages are still very low compared to previous years.

Even though bank lending rates haven’t fallen as much as base rates, mortgage payments are relatively low, and more attractive than renting.