Supply side policies are government policies which seek to increase the productivity and efficiency of the economy. They can involve interventionist supply side policies (e.g. government spending on education) or free market supply-side policies (e.g. reduce government legislation)

The main macroeconomic objectives of the government include:

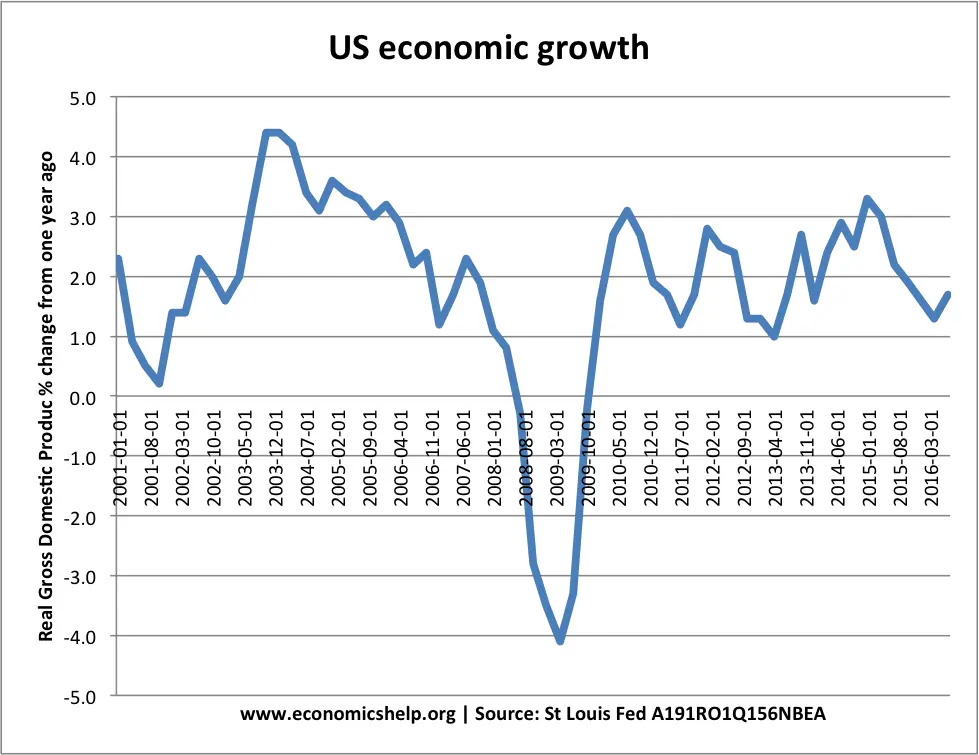

- Higher economic growth

- Low inflation

- Low unemployment

- Equilibrium on the balance of payments

Quite often these objectives conflict with each other. For example, expansionary fiscal policy may contribute to higher economic growth and lower unemployment; however, it will be at the cost of inflation and a deterioration on the current account.

To achieve all objectives simultaneously it is essential to improve the supply side of the economy. If the government can increase productivity and shift AS to the right, it can enable low inflationary growth and help improve the general competitiveness of the economy.

Long-run trend rate of economic growth

The main limitation for increasing the long-run trend rate of economic growth is the growth of productivity (output per worker). We cannot increase the long-run trend rate of growth through demand side policies. Therefore, if the government wants a higher sustainable rate of economic growth then it requires effective supply side policies which increase this productivity.

For example, effective training schemes which give workers more skills can lead to higher labour productivity. Governments could try and encourage firms to invest in more research and development by offering tax credits. If successful, these policies can enable countries to grow at a higher rate.

In practice, it is difficult for government supply side policies to improve the long-run trend rate of growth. Productivity growth depends to a large extent on technological improvements. These improvements mostly come independently of government policy.